First-time Homebuyers

Buying a house doesn't need to be scary...

Let's make it simple:

Download our Buyers Guide Now

What's included:

- More info about first-time homebuyer programs

- What closing costs and other moving fees are involved

- What to expect in the homebuying process

- Information on the local market

First-time homebuyer FAQs? We've got answers!

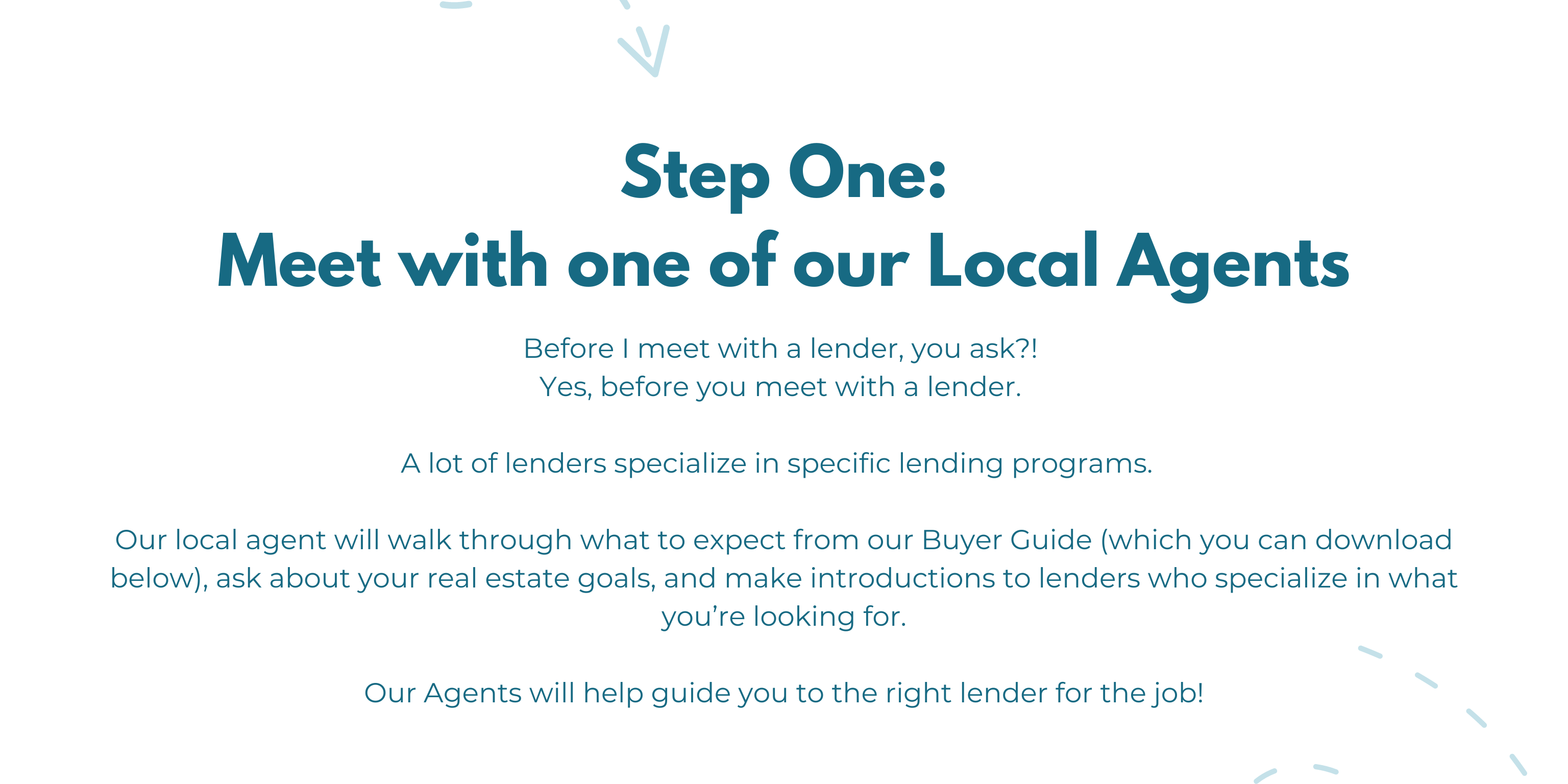

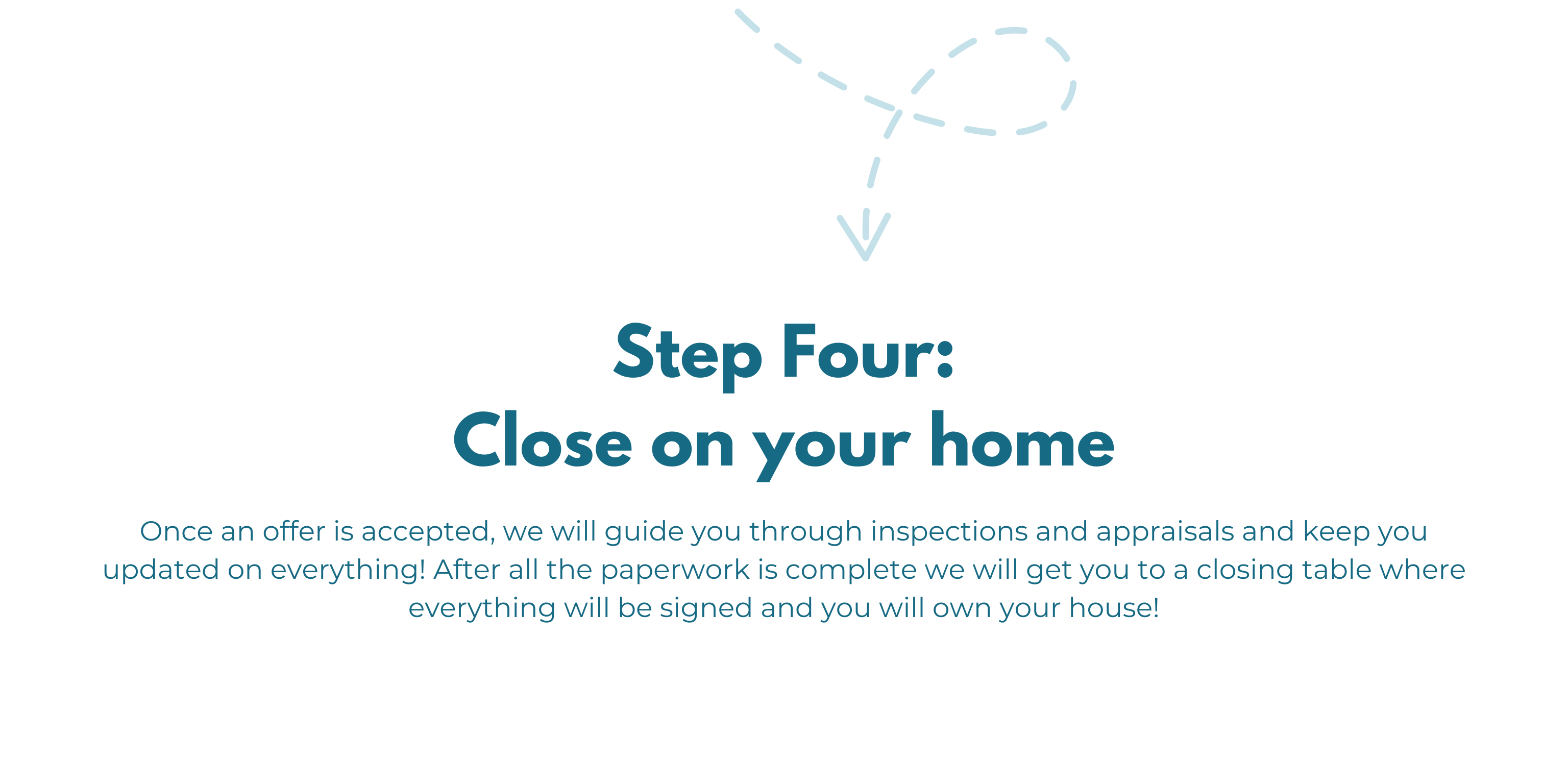

- Determine your budget and get pre-approved for a mortgage

- Find a real estate agent

- Search for homes and make an offer

- Have the home inspected

- Get a mortgage and close on the home

Get your finances in order: Before you start looking at homes, it’s a good idea to get a handle on your budget and credit score. You’ll need to provide proof of income and other financial documents when you apply for a mortgage, so having these things in order will make the process go more smoothly. It’s also a good idea to start saving for a down payment, which will typically be around 3-5% of the purchase price of the home.

Understand the different types of mortgages: There are a few different types of mortgages available to first-time homebuyers in Grand Rapids. A fixed-rate mortgage has an interest rate that stays the same over the life of the loan, while an adjustable-rate mortgage (ARM) has an interest rate that can change. You’ll also want to consider government-backed loans such as FHA loans, which can be a good option for first-time buyers with less-than-perfect credit.

Find a good real estate agent: A good real estate agent can be an invaluable resource for first-time buyers. They can help you navigate the process, answer your questions, and find homes that meet your needs and budget. When looking for an agent, it’s a good idea to get recommendations from friends or family, or to ask for referrals from a lender or mortgage broker.

Be prepared for the home inspection: A home inspection is an important part of the homebuying process. It’s a good idea to attend the inspection in person so you can see any issues or potential problems firsthand. The inspector will look at the condition of the home’s major systems and components, including the roof, foundation, and electrical and plumbing systems.

Don’t be afraid to ask for help: Buying a home can be overwhelming, especially if you’re doing it for the first time. It’s okay to ask for help or guidance from friends, family, or professionals such as real estate agents and mortgage brokers.

We hope this information is helpful as you start your journey as a first-time homebuyer in Grand Rapids. Good luck, and happy house hunting!

Michigan State Housing Development Authority (MSHDA): MSHDA offers a variety of programs to help first-time buyers in Michigan, including the MI First Home program, which provides down payment assistance of up to $7,500.

Kent County Land Bank Authority: The Kent County Land Bank Authority offers a down payment assistance program for first-time buyers in Kent County, which includes Grand Rapids. The program provides up to $5,000 in assistance.

Neighborhood Ventures: This program, offered by the Grand Rapids Community Foundation, provides down payment assistance of up to $15,000 for first-time buyers in Grand Rapids.

Grand Rapids Housing Commission: The Grand Rapids Housing Commission offers a down payment assistance program for first-time buyers in the city of Grand Rapids. The program provides up to $7,500 in assistance.

It’s important to note that these programs often have specific eligibility requirements and may only be available to buyers who meet certain income or credit score thresholds. It’s a good idea to check with the program directly to see if you qualify.

To determine how much you can afford to spend on a home, you should consider your income, debts, and any savings you have for a down payment. It is generally recommended to spend no more than 28-33% of your monthly income on housing expenses, including mortgage payments, property taxes, and insurance.

The amount you will need for a down payment depends on the type of mortgage you get and the price of the home you are purchasing. For conventional mortgages, you may need a down payment of at least 5% of the purchase price, while FHA loans may require as little as 3.5% down.

The type of mortgage you choose will depend on your financial situation and how long you plan to stay in the home. A fixed rate mortgage has an interest rate that stays the same for the entire loan term, while an adjustable rate mortgage (ARM) has an interest rate that can change over time. ARMs may have lower initial interest rates, but they can also be riskier if interest rates rise significantly.

A mortgage pre-approval is a letter from a lender indicating how much you are qualified to borrow for a home purchase. Having a pre-approval letter can make you a more competitive buyer and help you move faster when you find a home you want to purchase. To get a mortgage pre-approval, you will need to provide the lender with information about your income, debts, and credit history.

When looking for a real estate agent, you should look for someone who is knowledgeable about the local housing market and has experience working with first-time homebuyers. You should also look for an agent who is responsive, communicates clearly, and has a track record of success

To find a home that is right for you, start by making a list of your must-have features and desired location. Then, work with your real estate agent to search for homes that meet your criteria. Be sure to also consider the condition of the home and any repairs or renovations that may be needed.

A home inspection is a thorough examination of a home’s condition by a professional inspector. It is important to have a home inspection before purchasing a home to identify any potential issues or deficiencies that may not be immediately apparent. A home inspection can help you negotiate with the seller for repairs or credits, or give you the option to walk away from the sale if necessary.

Closing on a home involves signing the final documents and paying any remaining closing costs and fees. Before closing, you will typically review and sign a settlement statement that outlines all of the costs associated with the purchase of the home. You will also need to provide proof of homeowners insurance and any required funds for the down payment and closing costs.

A mortgage rate lock is an agreement between a lender and a borrower that guarantees a certain interest rate for a specified period of time, usually until the loan closes. A rate lock can protect you from rising interest rates and help you budget for your home purchase. However, it can also come with fees, and if rates drop, you may not be able to take advantage of the lower rates.

As of 2022, the median home price in Grand Rapids, MI is around $330,000. However, home prices can vary widely depending on factors such as location, size, and condition of the home.

Yes, there are several first-time homebuyer programs available in Grand Rapids, MI. These programs may offer assistance with down payments, closing costs, and other expenses. Some examples include the Michigan State Housing Development Authority (MSHDA) and the Grand Rapids Homeownership Center.

The property tax rate in Grand Rapids, MI is around 1.34%. This means that for every $100,000 of a home’s value, you can expect to pay around $1,340 in property taxes per year.

Some popular neighborhoods for first-time homebuyers in Grand Rapids, MI include Creston, East Hills, and Heritage Hill. These neighborhoods tend to have a mix of affordable homes and easy access to amenities and downtown Grand Rapids.